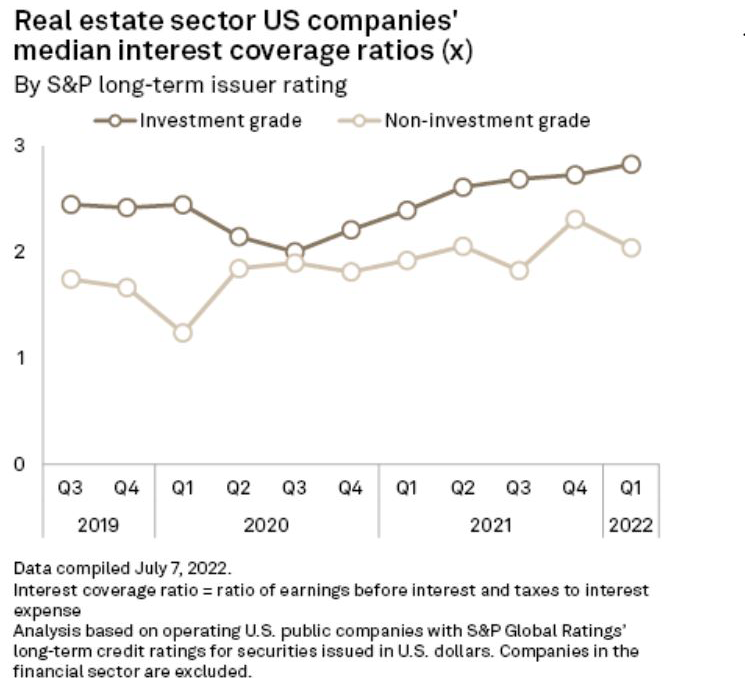

US Companies Continue to Reduce Debt Burdens

July 21, 2022 | Peter Brennan & Umer Khan | S&P Global Market Intelligence

Highly rated U.S. companies reduced their debt burdens in the first quarter of 2022, falling back on cash buffers built up during the pandemic rather than borrowing at rising interest rates.

The median interest coverage ratio for nonfinancial U.S. companies rated investment-grade by S&P Global Ratings rose to 8.3 in the first quarter of 2022, up from 8.1 in the fourth quarter of 2021, according to S&P Global Market Intelligence data. The ratio is a measure of a company’s ability to repay its debts calculated by dividing earnings before interest and taxes by the cost of debt-interest payments.

The ratio is down from the recent peak of 8.6 in the second quarter of 2021. It is markedly higher, however, than the pre-pandemic level of 6.1, suggesting that companies are still well positioned to manage their debts. The median ratio for non-investment-grade companies slipped to 4.0 from 4.1 but remained higher than the pre-pandemic level of 2.8.

The apparent health of corporate balance sheets is reinforced by median debt-to-equity ratios, a closely watched measurement of corporate leverage determined by calculating total liabilities as a percentage of shareholder equity.

The ratio for investment-grade-rated companies fell to 90.1% in the first three months of the year, down from 90.5% at the end of 2021, the eighth consecutive quarterly decline. Debt is significantly less of a burden than it was before the outbreak of COVID-19. The ratio was 93.6% in the fourth quarter of 2019.

Companies took advantage of cheap credit conditions created by the Federal Reserve’s pandemic stimulus by issuing record levels of bonds in 2020 and 2021, building up cash buffers, refinancing debt at lower rates and pushing out the maturities of those debts.

The cost of borrowing has risen in 2022 as inflation pushed the Fed to raise interest rates and wind down the quantitative easing program that infused cash into credit markets. But the strong cash positions of companies has allowed them to rein in issuance, reducing their exposure to higher rates.

Lower borrowing enabled companies in six of the 10 investment-grade sectors and five of the non-investment-grade-rated segments to increase their median interest coverage ratios in the first quarter of 2022.

There were some declines. For non-investment-grade-rated information technology companies, the median ratio fell to 5.8 from 6.9, while the non-investment-grade energy ratio fell to 2.6 from 5.3. Both were higher than the pre-pandemic level.

Most sectors have also lowered their debt-to-equity ratios over the course of the pandemic. Investment-grade-rated health care companies, for example, posted a median ratio of 70.2%, well below the pre-pandemic level of 82%.

The consumer discretionary sector stands alone in having raised its debt relative to equity since the COVID-19 outbreak. For investment-grade companies, the ratio is up to 137.3% from a pre-pandemic level of 118.1% — still significantly lower than the peak of 170.7% in 2020.