The Federal Reserve’s Double Whammy and Commercial Real Estate

May 4, 2022 | James Sprow | Blue Vault

Besides their intention to raise interest rates, the Fed is also planning to reduce its record balance sheet by selling off its assets which reached a record high during the pandemic as it pumped liquidity into the market. Now it’s time to deal with the four-decade high inflation its actions, along with the Federal government’s profligate spending, has caused. It won’t be easy.

According to Peter Brennan and Brian Scheid at S&P Capital Market Intelligence, “The Federal Reserve’s hawkish turn is exposing structural cracks in the bond market as the central bank pulls a historic level of accommodation from the marketplace.”

They continue, “The Fed provided critical support to the Treasury market during the COVID-19 pandemic, facilitating an explosion in the size of the market from $17.2 trillion to $23.8 trillion.”

The Fed’s Chairman Jerome Powell is expected to announce at least a 50-basis point rate hike this week. There will also be a planned reduction in the Fed’s balance sheet of more than $1.1 trillion per year. These two strategies are intended to stifle inflationary pressures by slowing the economy, which appears to be at full employment, but these actions may be too late to avoid sending the economy into recession.

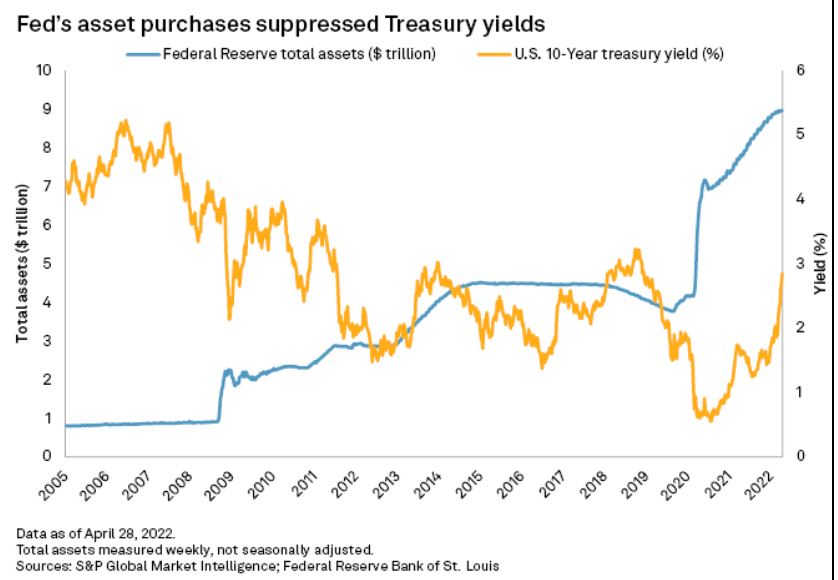

The above chart shows how extreme the Fed’s asset build up has been over the last two years, and how it suppressed Treasury yields by its purchases in the bond market. Ending that trend by off-loading bonds may very well stress the bond market so much that there is a danger in the supply of bonds over-powering the demand by major banks. As the supply of bonds exceeds demand by the private sector, bond prices will have to fall, raising interest rates further.

Observers point out that liquidity in the Treasury market is currently low when compared to the amount of supply coming to market as the Fed trims its balance sheet. Volatility is rising. Since 2011 the Fed’s balance sheet has been growing while the balance sheets of the largest banks have not kept pace. The question is whether the banks can absorb the supply of bonds that the Fed will be off-loading. Public Treasury holdings now dwarf the combined balance sheets of the largest U.S. banks. When the pandemic hit, bond investors sold off their holdings and the Fed’s massive bond-buying operations provided liquidity and held yields to historically low levels to stabilize markets and spur economic recovery. The Fed’s total assets rose from $4.2 trillion to almost $9 trillion. Now it’s time to pay the piper.

Implications for Commercial Real Estate

Commercial real estate investors have been locking in their long-term borrowing rates during the pandemic and are now looking at sectors where rents can keep up with or exceed inflation. Commercial real estate has historically been an excellent hedge against inflation, and even during recessions credit-worthy tenants have maintained both their rental payments and occupancies. Rent escalation clauses that raise rents at 2% annually or cap raises based upon changes in the CPI at 3% annually don’t look so attractive when recent inflation is at 8.5%. But real estate is a long-term investment and buyers are looking at the gaps between cap rates in the different sectors vs. the cost of debt. As long as cap rates exceed borrowing costs by a healthy margin, real estate will be a good investment. However, cap rate compression in some real estate sectors may make it more difficult to find attractive yields.

For example, a recent research report by Marcus & Millichap’s John Chang highlighted the differences between cap rates in the apartment sector and the 10-year Treasury yield (190 bps) and cap rates in the multi-tenant retail sector vs. the 10-year Treasury yield (380 bps). When those spreads reach the point where investors reconsider their portfolio strategies to take advantage of the higher risk-return tradeoffs to be found in different sectors, commercial real estate may offer higher expected total returns in sectors that suffered during the pandemic-induced slowdown. Retail assets in particular may benefit from the huge increase in savings and cash accounts that are held by consumers as they ramp up their buying. For the first time in three decades, U.S. households have more cash savings than debt and are primed to spend.

The top performing CRE sectors during the pandemic like Industrial, Multifamily and Self-Storage, may not be the sectors that out-perform going forward. Investors will be looking closely at Retail and Hospitality assets where cap rate spreads over 10-year Treasury yields are relatively high. Even if the Fed brings about a recession to tame inflation, over longer investment horizons those asset types may outperform.

Sources: S&P Global Market Intelligence, Marcus & Millichap