Rent Inflation Shows That Landlords Have the Upper Hand Again

February 1, 2022 | James Sprow | Blue Vault

The Federal Reserve’s rate hikes could add to upward pressure on residential leases.

If you’re a renter and you moved last year, you’re probably already paying more for shelter. If you didn’t, you may soon find yourself in a similar position, when your lease comes up for renewal.

Outsize residential rent increases spreading from new leases to existing ones has been a distinct pattern in places like the Atlanta and Detroit metro areas, where rents rose in 2021 at the fastest pace in decades, according to Labor Department data, propelled in part by an influx of new arrivals fleeing higher-cost cities. In 2022, the pattern is set to become a nationwide phenomenon, as landlords recoup bargaining power they lost in the early part of the pandemic, when unemployment surged and governments responded by enacting eviction bans.

Rent of shelter is the biggest expense for the typical U.S. household and consequently the biggest component of the government’s official indexes of consumer prices, making up about 32% of them by weight. Inflation in that category topped 4% in 2021, after averaging 3.3% annually in the five years before the pandemic.

Many forecasters expect it to remain high through much of this year, even as other overheated categories, such as autos and other durable goods, start moderating. (Several private-sector gauges of rent inflation showing double-digit growth nationally in 2021 focus on prices of new leases, whereas the Labor Department measure also accounts for the much larger category of existing leases being renewed.)

The trend may add to the impetus at the Federal Reserve for higher interest rates, though here the inflation cure could backfire. The reason: Rising mortgage costs could prevent some renters from becoming homeowners, putting additional pressure on the market.

It’s also the case that many of the forces driving rent inflation are either beyond the reach of or not immediately responsive to monetary policy. Among them is household formation, which initially dipped during the Covid-19 recession, but came roaring back soon thereafter as employment rebounded along with the economy.

“We’ve never seen as much demand as we saw in 2021, and now we have a severe lack of availability and low vacancy in all types of housing as well, and that’s really driving the rent inflation that we’re seeing,” says Jay Parsons, the head of economics at RealPage, Inc., a company that provides property-management software for landlords.

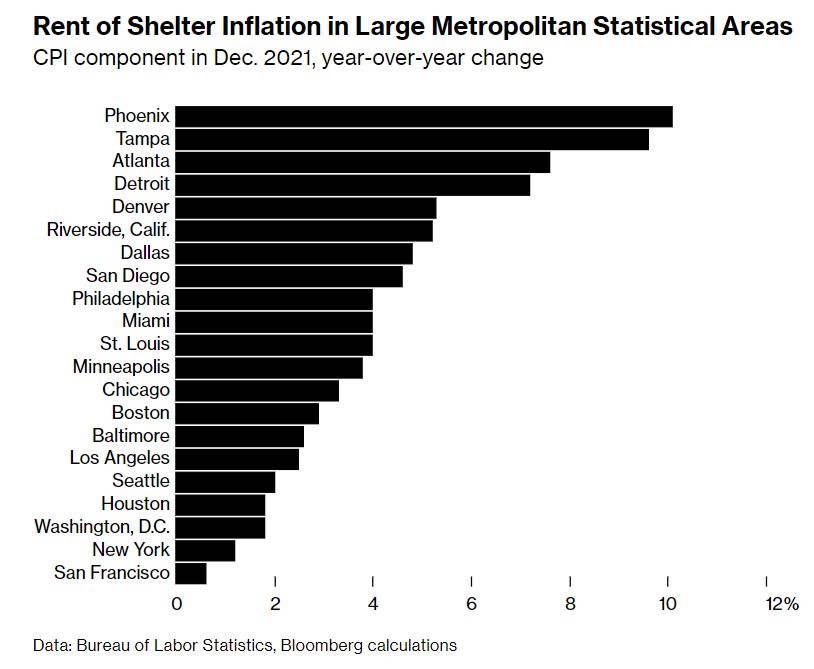

That’s especially so in cities like Phoenix, which logged a rent-of-shelter inflation rate last year of 10.1%, the highest among the major metros tracked by the Labor Department, according to Bloomberg calculations. But it’s yet to be reflected in some of the country’s largest and most expensive markets: Rents rose just 0.6% in the San Francisco metro area in 2021 and 1.2% in greater New York City.

U.S. Postal Service change-of-address records suggest people have over the past two years been fleeing cities with the highest cost of living for relatively more affordable ones, which helps explain why the latter have already seen rents surge, according to Paul Williams, a fellow at the Jain Family Institute.

“Right at the beginning of the pandemic, you see this radical shift, where the average rental cost in a city, if it’s higher than the U.S. median rent, people are just mass-exiting that city. And if it’s lower, people are mass-entering the city,” Williams says. “The places with the highest inflation right now are the ones that saw really significant demand shocks from changes in migration trends.”

Omair Sharif, president of the research firm Inflation Insights, sees rental inflation hitting multidecade highs of 5% or more later this year as rent increases spread to existing leases across the country. A pickup in building activity already underway should, by sometime in 2023, help bring it back down into the 3% to 4% range that prevailed before the pandemic. “We are seeing a pretty substantial supply response in some of these metros where we have seen big gains,” he says. “It’s just going take some time.”

Builders began construction on 1.6 million homes in 2021, the most since 2006. And they closed the year with momentum: Housing starts in December were the highest in nine months, led by groundbreaking of multifamily units. Completed projects are being rented out at an “historically fast pace,” according to the Joint Center for Housing Studies of Harvard University’s annual report on the U.S. rental housing market, published Jan. 21.

“By the second quarter of 2021, 72% of units were leased within three months of completion, up from 43% in the first quarter of 2020 and exceeding the 57% averaged from 2014 through 2021,” the report said. “The rapid pace of absorptions may encourage developers to continue building rental properties at today’s robust rate, potentially easing some of the pressure on supply.”

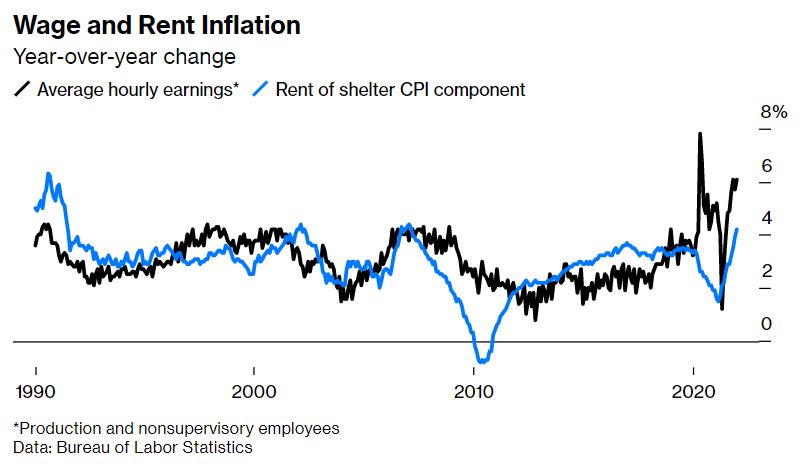

Rising incomes will help many renters cope with the higher rents. Average hourly earnings for production and nonsupervisory workers rose 5.8% in 2021, near the fastest pace since the early 1980s. Rental inflation tends to track wage growth over time because, as a landlord, “you’re not going to set your rents so high that no one could pay them,” Parsons says.

The averages obscure the very different experiences of renters on the low and high ends of the income spectrum. Moratoriums on evictions put in place in the earlier phases of the pandemic have begun to expire, and aid disbursed to help renters suffering loss of income is running out.

As a result, the U.S. is “seeing evictions trending up pretty much everywhere,” according to Carl Gershenson, a project director at Princeton University’s Eviction Lab. There could be more to come, especially in the metros seeing the biggest influx of new residents.

“There is some percentage of evictions that we would associate with turnover of lower-income renters for higher-income renters,” Gershenson says. “A lot of the Sun Belt and the Mountain West is going to experience displacement they haven’t dealt with before because of that,” he says. The concern is that, “whenever you have these cities experiencing displacement pressures, they sometimes don’t have the institutional or organizational infrastructure that larger cities have to deal with homelessness and displacement.”

Fed watchers expect the central bank to soon kick off the most aggressive string of interest-rate increases in decades in a bid to curb inflationary pressures. But this could prove counterproductive in taming rental inflation in particular, according to Carl Riccadonna, the chief industry economist at Bloomberg Intelligence.

“As the Fed tightens policy in an effort to cool inflation, shelter costs are likely to run counter to policymakers’ intentions—rising as the newly employed demand shelter and as higher interest rates slow construction and discourage home-buying,” Riccadonna said in a Jan. 26 report.

Source: Bloomberg Businessweek